Hello everyone, and welcome to another update of your friends at TrendSpider! In this update, we’ve made some really new and exciting changes to the Seasonality tool. If you have ever used the seasonal tool before, you know that it provides a visualization of how the stock has performed across different time periods; Monthly, weekly, daily and hourly. In this update, we’ve included some exciting new measurements that you can track right now. Details after the jump!

When you open the seasonality widget, you’ll notice a new dropdown next to the interval dropdown. It is preset to ‘change %> 0’ by default and can be seen checked in a red box in the image below.

When you click on that dropdown menu, you will see the following available options:

change %>0

This option shows us the percentage of time the stock has seen an increase in price.

Rel.Vol (20) > 1 or > 2

This option tells us the percentage of time a stock has had a relative volume value greater than 1 or 2, which means greater than its average volume or greater than 2x its average volume.

RSI (14) > 70 or 50

This option shows us the percentage of time the stock’s relative strength index (RSI) has been greater than 70 or 50, respectively.

RSI (14) <50 or 30

This option shows us the percentage of time the stock’s Relative Strength Index (RSI) has been below 50 or 30, respectively.

MFI (14) > 50 or less than 50

This option tells us the percentage of time that the MFI (Money Flow Index) was greater than or less than 50.

SMA (20) distance %> 0

This option shows us the percentage of time the stock has been trading above the 20-period simple moving average.

SMA(50) distance %>0

This option shows us the percentage of time the stock has been trading above the 50-period simple moving average.

SMA(100) distance %>0

This option shows us the percentage of time the stock has been trading above the 100-period simple moving average.

Take advantage of the new job

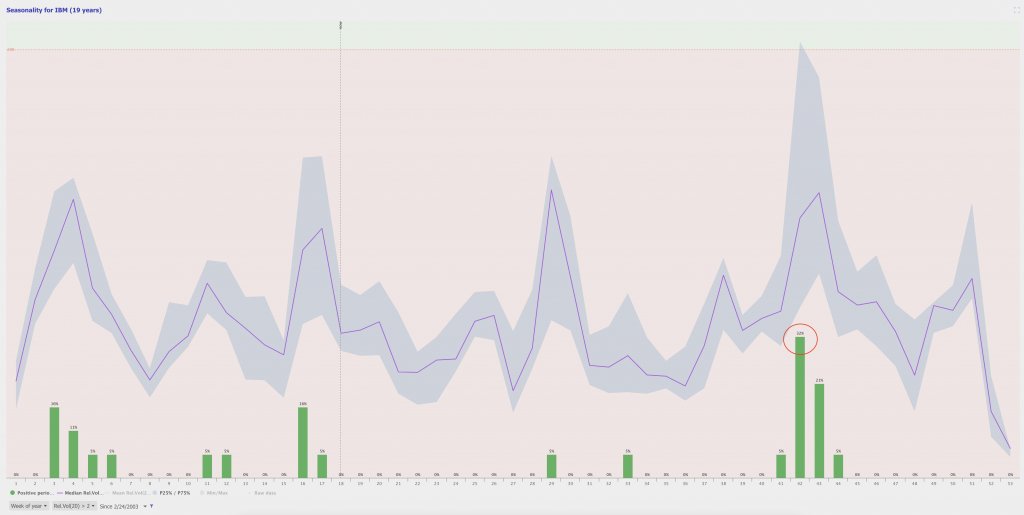

In the example below, we’re looking at relative volume on $IBM, specifically for weeks that were more than twice their average volume. Since 2003 we can clearly see that week 42 of the year tends to have the highest probability of seeing a 2x average volume. 32% of the time, to be exact!

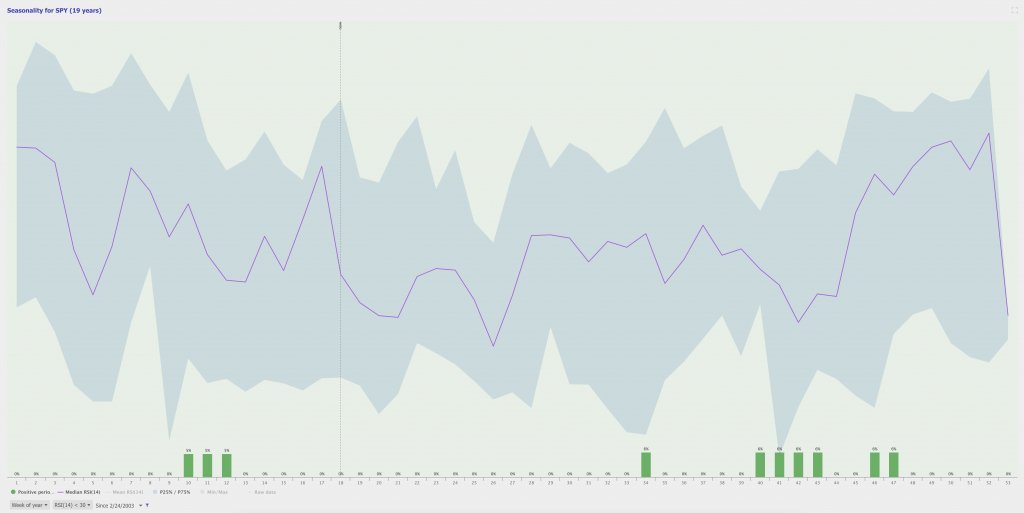

Next, we put our focus on the $spy and its relative reading. We have the ‘RSI(14)<30' option checked, which means we are looking for cases where the $SPY RSI is less than 30 on the weekly time frame. As you can see, it is very rare for this name to see the RSI below 30 on the weekly time frame. Since 2003, the highest at the time we saw this low RSI reading was 6%, and it tends to occur early in the year (weeks 10-12) and late in the year (weeks 34, 40-42, 46-47). . Since 2003, all other weeks have been closed with the RSI above 30.

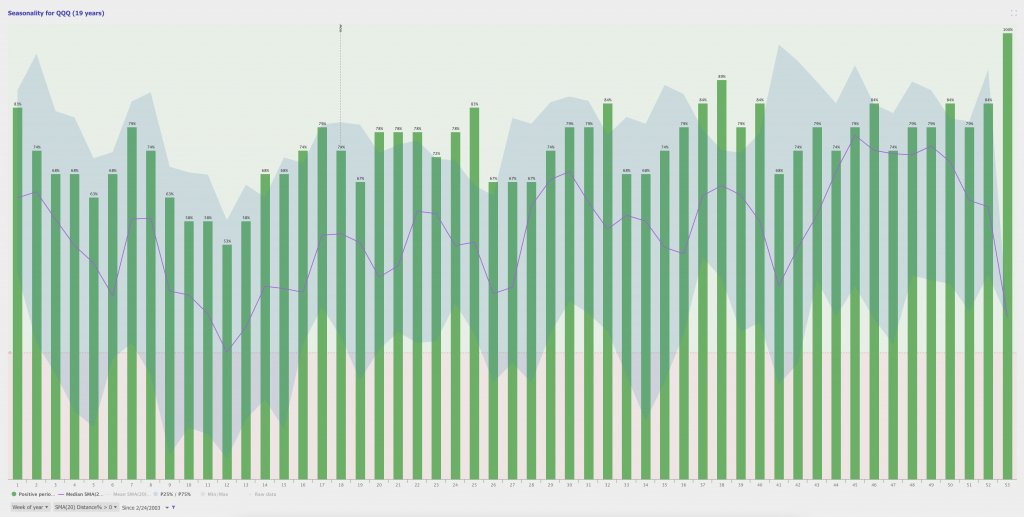

In the image below, we are looking at QQQ in USD, specifically the weeks of the year that it is trading above the 20 week simple moving average. As we can see, it traded 100% above the 20-week simple moving average during the last week of the year since 2003. Also note the 12th week of the year. This particular week, it has only traded above the 20-week simple moving average 53% of the time since 2003. This indicates that the end of March tends to be a poor time of the year for $QQQ.

We are really excited about this new update, and we have plans to add more functionality to the Seasonality tool in the future. We hope you find these new features useful and feel free to reach us via chat if you have any questions!

Leave a Reply